полная версия

полная версияThirty Years' View (Vol. II of 2)

"The bill comes to us now under more favorable auspices than it has ever done before. The President recommends it, and the Treasury needs the money which it will produce. A gentleman of the opposition [Mr. Clay], reproaches the President for inconsistency in making this recommendation; he says that he voted against it as senator heretofore, and recommends it as President now. But the gentleman forgets so tell us that Mr. Van Buren, when a member of the Senate, spoke in favor of the general object of the bill from the first day it was presented, and that he voted in favor of one degree of reduction – a reduction of the price of the public lands to one dollar per acre – the last session that he served here. Far from being inconsistent, the President, in this recommendation, has only carried out to their legitimate conclusions the principles which he formerly expressed, and the vote which he formerly gave.

"The bill, as modified on the motions of the senators from Tennessee and New Hampshire [Messrs. Grundy and Hubbard] stands shorn of half its original provisions. Originally it embraced four degrees of reduction, it now contains but two of those degrees. The two last – the fifty cent, and the twenty-five cent reductions, have been cut off. I made no objection to the motions of those gentlemen. I knew them to be made in a friendly spirit; I knew also that the success of their motions was necessary to the success of any part of the bill. Certainly I would have preferred the whole – would have preferred the four degrees of reduction. But this is a case in which the homely maxim applies, that half a loaf is better than no bread. By giving up half the bill, we may gain the other half; and sure I am that our constituents will vastly prefer half to nothing. The lands may now be reduced to one dollar for those which have been five years in market, and to seventy-five cents for those which have been ten years in market. The rest of the bill is relinquished for the present, not abandoned for ever. The remaining degrees of reduction will be brought forward hereafter, and with a better prospect of success, after the lands have been picked and culled over under the prices of the present bill. Even if the clauses had remained which have been struck out, on the motions of the gentlemen from Tennessee and New Hampshire, it would have been two years from December next, before any purchases could have been made under them. They were not to take effect until December, 1840. Before that time Congress will twice sit again; and if the present bill passes, and is found to work well, the enactment of the present rejected clauses will be a matter of course.

"This is a measure emphatically for the benefit of the agricultural interest – that great interest, which he declared to be the foundation of all national prosperity, and the backbone, and substratum of every other interest – which was, in the body politic, front rank for service, and rear rank for reward – which bore nearly all the burthens of government while carrying the government on its back – which was the fountain of good production, while it was the pack-horse of burthens, and the broad shoulders which received nearly all losses – especially from broken banks. This bill was for them; and, in voting for it, he had but one regret, and that was, that it did not go far enough – that it was not equal to their merits."

The bill passed by a good majority – 27 to 16; but failed to be acted upon in the House of Representatives, though favorably reported upon by its committee on the public lands.

2. The pre-emptive system. The provisions of the bill were simple, being merely to secure the privilege of first purchase to the settler on any lands to which the Indian title had been extinguished; to be paid for at the minimum price of the public lands at the time. A senator from Maryland, Mr. Merrick, moved to amend the bill by confining its benefits to citizens of the United States – excluding unnaturalized foreigners. Mr. Benton opposed this motion, in a brief speech.

"He was entirely opposed to the amendment of the senator from Maryland (Mr. Merrick). It proposed something new in our legislation. It proposed to make a distinction between aliens and citizens in the acquisition of property. Pre-emption rights had been granted since the formation of the government; and no distinction, until now, had been proposed, between the persons, or classes of persons, to whom they were granted. No law had yet excluded aliens from the acquisition of a pre-emption right, and he was entirely opposed to commencing a system of legislation which was to affect the property rights of the aliens who came to our country to make it their home. Political rights rested on a different basis. They involved the management of the government, and it was right that foreigners should undergo the process of naturalization before they acquired the right of sharing in the government. But the acquisition of property was another affair. It was a private and personal affair. It involved no question but that of the subsistence, the support, and the comfortable living of the alien and his family. Mr. B. would be against the principle of the proposed amendment in any case, but he was particularly opposed to this case. Who were the aliens whom it proposed to affect? Not those who are described as paupers and criminals, infesting the purlieus of the cities, but those who had gone to the remote new States, and to the remote parts of those States, and into the depths of the wilderness, and there commenced the cultivation of the earth. These were the description of aliens to be affected; and if the amendment was adopted, they would be excluded from a pre-emption right in the soil they were cultivating, and made to wait until they were naturalized. The senator from Maryland (Mr. Merrick), treats this as a case of bounty. He treats the pre-emption right as a bounty from the government, and says that aliens have no right to this bounty. But, is this correct? Is the pre-emption a bounty? Far from it. In point of money, the pre-emptioner pays about as much as any other purchaser. He pays the government price, one dollar and twenty-five cents; and the table of land sales proves that nobody pays any more, or so little more that it is nothing in a national point of view. One dollar twenty-seven and a half cents per acre is the average of all the sales for fifteen years. The twenty millions of acres sold to speculators in the year 1836, all went at one dollar and twenty-five cents per acre. The pre-emption then is not a bounty, but a sale, and a sale for full price, and, what is more, for solid money; for pre-emptioners pay with gold and silver, and not with bank credits. Numerous were the emigrants from Germany, France, Ireland, and other countries, now in the West, and especially in Missouri, and he (Mr. B.) had no idea of imposing any legal disability upon them in the acquisition of property. He wished them all well. If any of them had settled upon the public lands, so much the better. It was an evidence of their intention to become citizens, and their labor upon the soil would add to its product and to the national wealth."

The motion of Mr. Merrick was rejected by a majority of 13. The yeas were: Messrs. Bayard, Clay of Kentucky, Clayton, Crittenden, Davis, Knight, Merrick, Prentiss, Preston, Rives, Robbins, Smith, of Indiana, Southard, Spence, Tallmadge, Tipton, 15. The nays were: Messrs. Allen, Benton, Brown, Buchanan, Calhoun, Clay, of Alabama, Cuthbert, Fulton, Grundy, Hubbard, King, Linn, Lumpkin, Lyon, Mouton, Nicholas, Niles, Nowell, Pierce, Roane, Robinson, Sevier, Walker, Webster, White, Williams, Wright, Young, of Illinois, (28.) The bill being then put to the vote, was passed by a majority of 14.

3. Taxation of public lands when sold. When the United States first instituted their land system, the sales were upon credit, at a minimum price of two dollars, payable in four equal annual payments, with a liability to revert if there should be any failure in the payments. During that time it was considered as public land, nor was the title passed until the patent issued – which might be a year longer. Five years, therefore, was the period fixed, during which the land so sold should be exempt from taxation by the State in which it lay. This continued to be the mode of sale, until the year 1821, when the credit was changed for the cash system, and the minimum price reduced to one dollar twenty-five cents per acre. The reason for the five years exemption from state taxation had then ceased, but the compacts remaining unaltered, the exemption continued. Repeated applications were made to Congress to consent to the modification of the compacts in that article; but always in vain. At this session the application was renewed on the part of the new States; and with success in the Senate, where the bill for that purpose passed nearly unanimously, the negatives being but four, to wit: Messrs. Brown, Clay of Kentucky, Clayton, Southard. Being sent to the H. R. it remained there without action till the end of the session.

CHAPTER XXXI.

SPECIE BASIS FOR BANKS: ONE THIRD OF THE AMOUNT OF LIABILITIES THE LOWEST SAFE PROPORTION: SPEECH OF MR. BENTON ON THE RECHARTER OF THE DISTRICT BANKS

This is a point of great moment – one on which the public mind has not been sufficiently awakened in this country, though well understood and duly valued in England. The charters of banks in the United States are usually drawn on this principle, that a certain proportion of the capital, and sometimes the whole of it, shall be paid up in gold or silver before the charter shall take effect. This is the usual provision, without any obligation on the bank to retain any part of this specie after it gets into operation; and this provision has too often proved to be illusory and deceptive. In many cases, the banks have borrowed the requisite amount for a day, and then returned it; in many other cases, the proportion of specie, though paid up in good faith, is immediately lent out, or parted with. The result to the public is about the same in both cases; the bank has little or no specie, and its place is supplied by the notes of other banks. The great vice of the banking system in the United States is in banking upon paper – upon the paper of each other – and treating this paper as cash. This may be safe among the banks themselves; it may enable them to settle with one another, and to liquidate reciprocal balances; but to the public it is nothing. In the event of a run upon a bank, or a general run upon all banks, it is specie, and not paper, that is wanted. It is specie, and not paper, which the public want, and must have.

The motion of the senator from Pennsylvania [Mr. Buchanan] is intended to remedy this vice in these District banks; it is intended to impose an obligation on these banks to keep in their vaults a quantum of specie bearing a certain proportion to the amount of their immediate liabilities in circulation and deposits. The gentleman's motion is well intended, but it is defective in two particulars: first, in requiring the proportion to be the one-fourth, instead of the one-third, and next, in making it apply to the private deposits only. The true proportion is one-third, and this to apply to all the circulation and deposits, except those which are special. This proportion has been fixed for a hundred years at the Bank of England; and just so often as that bank has fallen below this proportion, mischief has occurred. This is the sworn opinion of the present Governor of the Bank of England, and of the directors of that institution. Before Lord Althorpe's committee in 1832, Mr. Horsley Palmer, the Governor of the Bank, testified in these words:

"'The average proportion, as already observed, of coin and bullion which the bank thinks it prudent to keep on hand, is at the rate of a third of the total amount of all her liabilities, including deposits as well as issues.' Mr. George Ward Norman, a director of the bank, states the same thing in a different form of words. He says: 'For a full state of the circulation and the deposits, say twenty-one millions of notes and six millions of deposits, making in the whole twenty-seven millions of liabilities, the proper sum in coin and bullion for the bank to retain is nine millions.' Thus, the average proportion of one-third between the specie on hand and the circulation and deposits, must be considered as an established principle at that bank, which is quite the largest, and amongst the oldest – probably, the very oldest bank of circulation in the world."

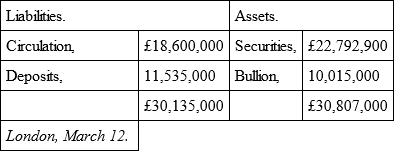

The Bank of England is not merely required to keep on hand, in bullion, the one-third of its immediate liabilities; it is bound also to let the country see that it has, or has not, that proportion on hand. By an act of the third year of William IV., it is required to make quarterly publications of the average of the weekly liabilities of the bank, that the public may see whenever it descends below the point of safety. Here is the last of these publications, which is a full exemplification of the rule and the policy which now governs that bank:

Quarterly average of the weekly liabilities and assets of the Bank of England, from the 12th December, 1837, to the 6th of March, 1838, both inclusive, published pursuant to the act 3 and William IV., cap. 98:

According to this statement, the Bank of England is now safe; and, accordingly, we see that she is acting upon the principle of having bullion enough, for she is shipping gold to the United States.

The proportion in England is one-third. The bank relies upon its debts and other resources for the other two-thirds, in the event of a run upon it. This is the rule in that bank which has more resources than any other bank in the world; which is situated in the moneyed metropolis of the world – the richest merchants its debtors, friends and customers – and the Government of England its debtor and backer, and always ready to sustain it with exchequer bills, and with every exertion of its credit and means. Such a bank, so situated and so aided, still deems it necessary to its safety to keep in hand always the one-third in bullion of the amount of its immediate liabilities. Now, if the proportion of one-third is necessary to the safety of such a bank, with such resources, how is it possible for our banks, with their meagre resources and small array of friends, to be safe with a less proportion?

This is the rule at the Bank of England, and just as often as it has been departed from, the danger of that departure has been proved. It was departed from in 1797, when the proportion sunk to the one-seventh; and what was the result? The stoppage of the banks, and of all the banks in England, and a suspension of specie payments for six-and-twenty years! It was departed from again about a year ago, when the proportion sunk to one-eighth nearly; and what was the result? A death struggle between the paper systems of England and the United States, in which our system was sacrificed to save hers. Her system was saved from explosion! but at what cost? – at what cost to us, and to herself? – to us a general stoppage of all the banks for twelve months; to the English, a general stagnation of business, decline of manufactures, and of commerce, much individual distress, and a loss of two millions sterling of revenue to the Crown. The proportion of one-third may then be assumed as the point of safety in the Bank of England; less than that proportion cannot be safe in the United States. Yet the senator from Pennsylvania proposes less – he proposes the one-fourth; and proposes it, not because he feels it to be the right proportion, but from some feeling of indulgence or forbearance to this poor District. Now, I think that this is a case in which kind feelings can have no place, and that the point in question is one upon which there can be no compromise. A bank is a bank, whether made in a district or a State; and a bank ought to be safe, whether the stockholders be rich or poor. Safety is the point aimed at, and nothing unsafe should be tolerated. There should be no giving and taking below the point of safety. Experienced men fix upon the one-third as the safe proportion; we should not, therefore, take a less proportion. Would the gentleman ask to let the water in the boiler of a steamboat sink one inch lower, when the experienced captain informed him that it had already sunk as low as it was safe to go? Certainly not. So of these banks. One-third is the point of safety; let us not tamper with danger by descending to the one-fourth.

When a bank stops payment, the first thing we see is an exposition of its means, and a declaration of ultimate ability to pay all its debts. This is nothing to the holders of its notes. Immediate ability is the only ability that is of any avail to them. The fright of some, and the necessity of others, compel them to part with their notes. Cool, sagacious capitalists can look to ultimate ability, and buy up the notes from the necessitous and the alarmed. To them ultimate ability is sufficient; to the community it is nothing. It is, therefore, for the benefit of the community that the banks should be required to keep always on hand the one-third of their circulation and deposits; they are then trusted for two-thirds, and this is carrying credit far enough. If pressed by a run, it is as much as a bank can do to make up the other two-thirds out of the debts due to her. Three to one is credit enough, and it is profit enough. If a bank draws interest upon three dollars when it has but one, this is eighteen per cent., and ought to content her. A citizen cannot lend his money for more than six per cent., and cannot the banks be contented with eighteen? Must they insist upon issuing four dollars, or even five, upon one, so as to draw twenty-four or thirty per cent.; and thus, after paying their officers vast salaries, and accommodating friends with loans on easy terms, still make enough out of the business community to cover all expenses and all losses: and then to divide larger profits than can be made at any other business?

The issuing of currency is the prerogative of sovereignty. The real sovereign in this country – the government – can only issue a currency of the actual dollar: can only issue gold and silver – and each piece worth its face. The banks which have the privilege of issuing currency issue paper; and not content with two more dollars out for one that is, they go to five, ten, twenty – failing of course on the first run; and the loss falling upon the holders of its notes – and especially the holders of the small notes.

We now touch a point, said Mr. B., vital to the safety of banking, and I hope it will neither be passed over without decision, nor decided in an erroneous manner. We had up the same question two years ago, in the discussion of the bill to regulate the keeping of the public moneys by the local deposit banks. A senator from Massachusetts (Mr. Webster) moved the question; he (Mr. B.) cordially concurred in it; and the proportion of one-fourth was then inserted. He (Mr. B.) had not seen at that time the testimony of the governor and directors of the Bank of England, fixing on the one-third as the proper proportion, and he presumed that the senator from Massachusetts (Mr. W.) had not then seen it, as on another occasion he quoted it with approbation, and stated it to be the proportion observed at the Bank of the United States. The proportion of one-fourth was then inserted in the deposit bill; it was an erroneous proportion, but even that proportion was not allowed to stand. After having been inserted in the bill, it was struck out; and it was left to the discretion of the Secretary of the Treasury to fix the proportion. To this I then objected, and gave my reasons for it. I was for fixing the proportion, because I held it vital to the safety of the deposit banks; I was against leaving it to the secretary, because it was a case in which the inflexible rule of law, and not the variable dictate of individual discretion should be exercised; and because I was certain that no secretary could be relied upon to compel the banks to toe the mark, when Congress itself had flinched from the task of making them do it. My objections were unavailing. The proportion was struck out of the bill; the discretion of the secretary to fix it was substituted; and that discretion it was impossible to exercise with any effect over the banks. They were, that is to say, many of them were, far beyond the mark then; and at the time of the issuing of the Treasury order in July, 1836, there were deposit banks, whose proportion of specie in hand to their immediate liabilities was as one to twenty, one to thirty, one to forty, and even one to fifty! The explosion of all such banks was inevitable. The issuing of the Treasury order improved them a little: they began to increase their specie, and to diminish their liabilities; but the gap was too wide – the chasm was too vast to be filled: and at the touch of pressure, all these banks fell like nine-pins! They tumbled down in a heap, and lay there, without the power of motion, or scarcely of breathing. Such was the consequence of our error in omitting to fix the proper proportion of specie in hand to the liabilities of our deposit banks: let us avoid that error in the bill now before us.

CHAPTER XXXII.

THE NORTH AND THE SOUTH: COMPARATIVE PROSPERITY: SOUTHERN DISCONTENT: ITS TRUE CAUSE

To show the working of the federal government is the design of this View – show how things are done under it and their effects; that the good may be approved and pursued, the evil condemned and avoided, and the machine of government be made to work equally for the benefit of the whole Union, according to the wise and beneficent intent of its founders. It thus becomes necessary to show its working in the two great Atlantic sections, originally sole parties to the Union – the North and the South – complained of for many years on one part as unequal and oppressive, and made so by a course of federal legislation at variance with the objects of the confederation and contrary to the intent or the words of the constitution.

The writer of this View sympathized with that complaint; believed it to be, to much extent, well founded; saw with concern the corroding effect it had on the feelings of patriotic men of the South; and often had to lament that a sense of duty to his own constituents required him to give votes which his judgment disapproved and his feelings condemned. This complaint existed when he came into the Senate; it had, in fact, commenced in the first years of the federal government, at the time of the assumption of the State debts, the incorporation of the first national bank, and the adoption of the funding system; all of which drew capital from the South to the North. It continued to increase; and, at the period to which this chapter relates, it had reached the stage of an organized sectional expression in a voluntary convention of the Southern States. It had often been expressed in Congress, and in the State legislatures, and habitually in the discussions of the people; but now it took the more serious form of joint action, and exhibited the spectacle of a part of the States assembling sectionally to complain formally of the unequal, and to them, injurious operation of the common government, established by common consent for the common good, and now frustrating its object by departing from the purposes of its creation. The convention was called commercial, and properly, as the grievance complained of was in its root commercial, and a commercial remedy was proposed.

It met at Augusta, Georgia, and afterwards at Charleston, South Carolina; and the evil complained of and the remedy proposed were strongly set forth in the proceedings of the body, and in addresses to the people of the Southern and Southwestern States. The changed relative condition of the two sections of the country, before and since the Union, was shown in their general relative depression or prosperity since that event, and especially in the reversed condition of their respective foreign import trade. In the colonial condition the comparison was wholly in favor of the South; under the Union wholly against it. Thus, in the year 1760 – only sixteen years before the Declaration of Independence – the foreign imports into Virginia were £850,000 sterling, and into South Carolina £555,000; while into New York they were only £189,000, into Pennsylvania £490,000; and into all the New England Colonies collectively only £561,000.